A valuable resource for:

- making informed business and tech adoption decisions

- becoming best in class at quote-to-cash

- keeping up with and adopting best practices

The go-to research and advisory resource for monetization leaders.

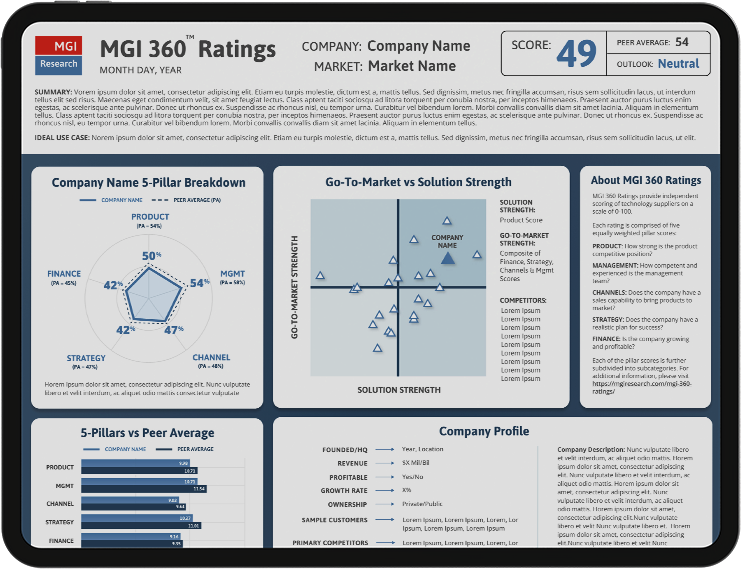

This comprehensive report rates leading CLM suppliers by their product functionality, management teams, channel breadth, marketing strategy, financial positioning, and more.

In this session, Conga CPO (and former DocuSign CTO) Grant Peterson joins MGI analysts to explore the transformative potential of AI within the Contract Lifecycle Management (CLM) landscape.

is an independent research and strategic advisory firm focused on the needs of technology buyers, vendors, and institutional investors.

MGI is defined by its distinctly quantitative, forthright, and focused approach to answering questions that actually impact the bottom line. We provide unique value to our clients through various means including:

Subscription-Based Research

A valuable resource for:

Vendor Ratings

Impactful guides for:

Market Forecasts

The industry’s preferred choice for:

Advisory Engagements

A trusted partner in:

Looking for ways to eliminate customer friction and break from the pack?

MGI analysts have decades of experience providing independent advice and identifying new strategies to drive growth.

Looking to efficiently find suppliers that fit your needs without cutting corners?

MGI’s impartial, in-depth methodology will help you reduce risk and zero in on your best fit.

Looking to eliminate revenue leakage and optimize your quote to cash process?

MGI analysts are first-rate partners in sales cycle improvements, which can increase revenues by 2-4%.

Searching for sustainable differentiation within your TAM?

MGI’s unmatched industry research will provide prescient market data and unique insights.

Want to understand the hidden levers of durable valuation improvement?

MGI Forecasts have been used to raise billions and to sharpen ABM strategies.

Need to size up a market with more than just a huge number and pivot table?

MGI’s account-based forecasting tool allows you to tap into company-level spend.

Looking to separate hype from durable trends in the market?

Access an unbiased sounding board that can validate assumptions and test hypotheses.

Searching for tomorrow’s winners and outliers?

Get a 360 view of which products and teams will outperform.

Need to save time and mitigate risk in the opportunity sourcing process?

MGI will help you connect with quality investable opportunities.

This report compares CLM suppliers to their direct competitors in terms of agility, complexity, volume, solution strength, and go-to-market strength.

This Buyer's Guide to the Contract Lifecycle Management market rates leading suppliers and explores the evolution of CLM as a discipline.

This research note explores how companies can grow their global sales without compromising time-to-market, customer experience, and brand control.